Why US lags behind EU in instant bank-to-bank transfers

So that you can stop just nodding along when fintech people remind you of this fact

Damp from standing in the Copenhagen rain to get my lunch, and sweaty from wearing a wool sport jacket, I wasn’t entirely comfortable sitting in breakout room number one. I was at Nordic Fintech Week watching a panel discussion about how to work towards a “Big Vision” of the future within fintech.

The speakers on the panel were successful, composed, intelligent, and assumed the audience shared their understanding of the market. At one point, one of the speakers, a fintech founder and CEO, made mention of the progress Europe has made in instant bank to bank transfers, and with a knowing look toward the audience, he said, “We find ourselves a bit ahead of the US in this regard.”

The audience collectively nodded. Everyone was in on it. It goes without saying, or explaining, that Europe’s banking and payments technology is significantly more advanced than that of the United States. But, as many times as I had heard this, since no one had ever explained it to me, I had no idea why.

I decided to find out. I would start with the much narrower question of why Europe has made good progress on instant bank to bank transfer and the United States has not. I started my search on Google looking for a quick ‘splainer, but it turned into a rabbit hole.

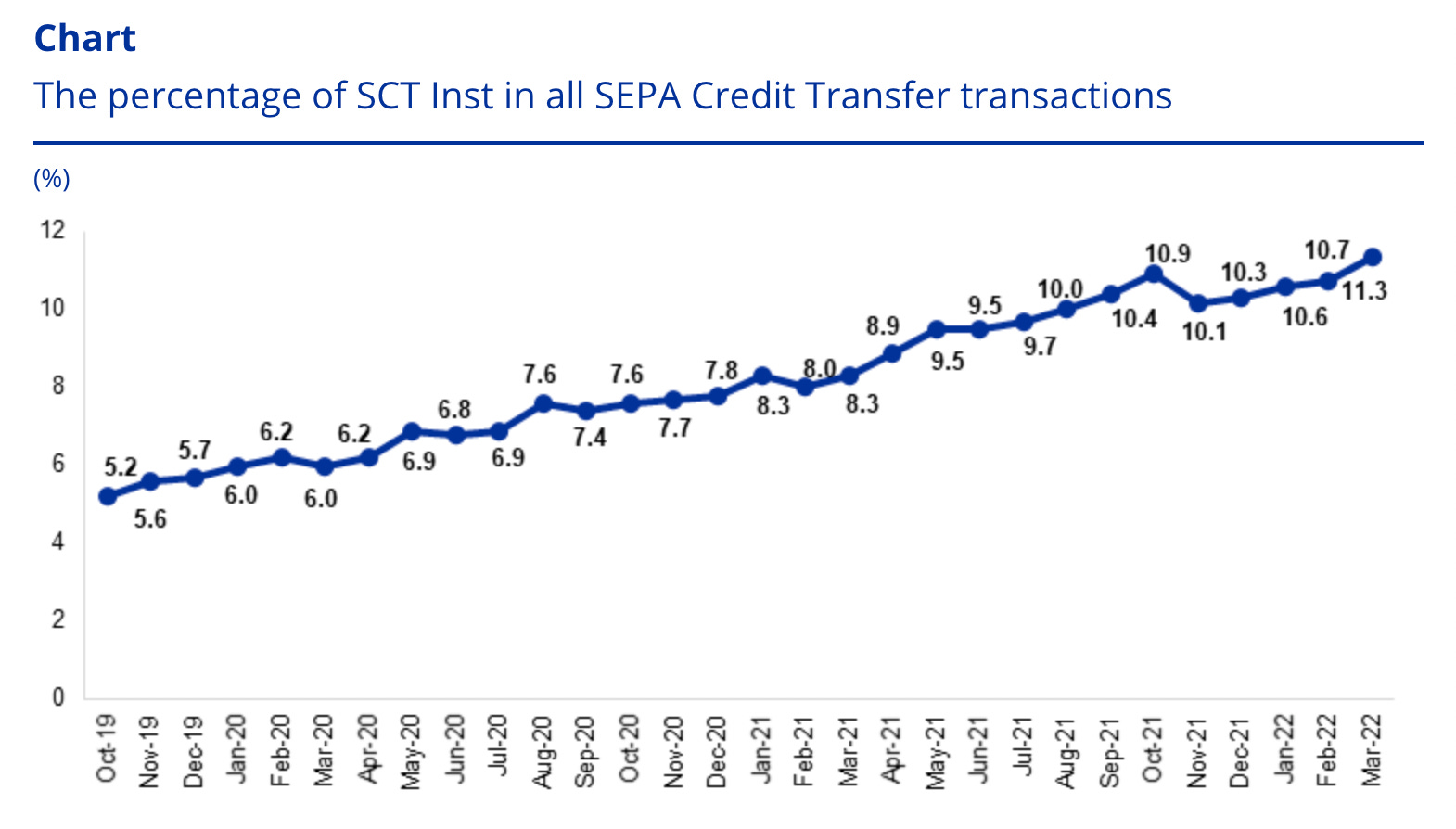

First, let’s not just take my word for it that instant bank to bank transfer is further along in the EU than in the US. Here’s a chart of progress in the EU:

Here’s a related chart for the US

Put into context, that $20 billion dollar number looks small at less than 1% of total payment volume in 2021:

In my journey down the rabbit hole, I found three reasons for the discrepancy in payment technology and bank behavior between the US and EU. First, the EU had direct and pressing needs for significant changes in banking as it went form a model of every country for itself to a unified economy in during the aughts. Second, large banks’ resistance to change and regulation is present in the EU, but has been less successful than in the US, where it’s very powerful. And finally, there have been a few key influential and motivated policymakers doing effective leadership in the EU.

The European banking and payments garden was already well tilled

The first reason, that the EU was coming together and needed to change the way it did banking, is rather obvious now that I understand it. Without getting deeply into the reasons that the EU was formed in the first place, we can agree that EU nations were looking for global advantages working as a single unit. Working as a unit necessarily included the way member nations conduct banking and finance, and the most powerful example of that was the formation of the Euro as a single currency that most EU nations adopted. Near the same time as the creation of the Euro, the European Commission, EU’s government branch that proposes new laws and enforces existing ones, set out a vision of a single European payment area, which they dubbed SEPA.

European banks, realizing that they would be forced into action by the new EU government, chose to work together to combine their power into a strong lobbying and policy guiding force called the European Payments Commission (EPC) founded in ‘02. The EPC saw to the details of creating new cross border payments schemes, surely with the interests of the member banks in mind.

If things had stopped there, the EU and US would look similar in terms of payments technology. EU banks would be able to inexpensively send money to each other using newer but functionally similar transit rails to US ACH payments, with easily routable batch transactions and settlement requiring at least a day. Further changes to interbank payments would have been tightly controlled by the EPC and its member banks would have retained their incumbent advantages.

Politics and the power differential between banking coalitions in the US vs the EU

But things didn’t stop there. The EU has recently enjoyed a period of strong political will in favor of robust regulation owing to, among other things, preferences of policy elites, and the administrative and legal criteria for assessing risk. In banking and payments, therefore, the EU had policy experts wanting to sew the seeds of payments innovation—who we will discuss in a moment—and a political environment in Parliament that could pass laws that would create high implementation costs for existing banking institutions in order to protect consumers and promote fair competition.

Contrast that with the political situation in the US where neither of the two political parties can accumulate enough votes in the chambers of Congress to pass new laws, and every issue, regardless of topic or public opinion lands squarely along party lines.

Given this lack of political will in the US to apply new regulations to payments or banking activity, the future is determined by existing powerful banks. When they need to interoperate, they create coalitions to make changes in lockstep while gatekeeping and protecting their market positions. US banks have created these coalitions in response to multiple financial innovations from real time payments (RTP) to cryptocurrencies. The RTP coalition is called The Clearing House and despite benevolent sounding language on its home page claiming to welcome “all federally insured U.S. depository institutions,” its 25 owner banks are statutorily acting to maximize shareholder value for their own institutions which means protecting themselves from competition.

The 77 member banks of the European Payments Commission would likely have arranged Europe’s future of banking and payments in the same anti-competitive way as those in The Clearing House had it not been for some strong leadership from policy makers in the European Commission. Wired magazine did an excellent deep dive on Open Banking in 2017 which I will draw from to highlight the importance of individual policymakers in creating the modern fintech environment in the EU.

The two leaders behind the EU payments and Open Banking transformation

Open Banking was shepherded in by a law called PSD2 which was passed in 2016. It had three main parts.

Requirements for strong (multi-factor) authentication for customers to access bank information and initiate payments.

Establishment of improved bank to bank transfer capabilities within the Eurozone that are interoperable with third party payments providers (this is the part that leads to instant transfers).

Ensuring banks create standardized APIs for third party applications to retrieve product and customer data.

Even though this post is about why the EU has instant bank to bank transfers and the US mostly doesn’t, it’s the third piece of the PSD2 law that is most astonishing. Having witnessed the power of big business lobbying groups on Washington, I can’t wrap my head around the audacity and power of the the Open Banking rule. Big Banks maintain their position by integrating their ownership of customer information and deposits. Forcing them to open up that information to third parties without charging for it is astounding and transformative.

Apparently, the open banking idea was the brainchild of a guy named John Gibson who was excited in the early 2010’s by innovation in other markets with the emergence of data rich APIs like the Google Maps API. He wanted the equivalent of an App Store for banking, and wrote a report for the European Treasury about how it could work.

The result of Gibson’s work is called The Fingleton Report, a thoughtful, and surprisingly readable breakdown of what could be made possible with Open Banking and how to get there. He published it with with Andy Reiss as an independent report for the UK government in 2014. The UK government’s Competition and Markets Authority (CMA) took the study and started running with it. It was a blueprint for banking disruption to be carried out by the banks themselves.

After the PSD2 law was passed and Open Banking turned from a vision to a project in need of implementation, a fintech founder and operator named Imran Gulamhuseinwala was put in charge of the UK’s Open Banking Limited, the organization with the mandate to steward implementation of Open Banking. There, he established himself as a forceful leader working against the inertial stasis of the big banks to get them to develop open and useful APIs.

In his interview with Wired, Gulamhuseinwala talked about how banks had been dragging their feet to begin implementation and were wanting to do the minimum necessary for compliance. One of their largest sources of income, overdraft fees, was on the line because Open Banking would allow third parties to create tools that would warn customers and prevent them from making costly unexpected overdrafts.

But to Gulamhuseinwala’s apparent surprise, and perhaps because the banks already saw the writing on the wall for overdraft fees when the The Financial Conduct Authority listed them as a source of “significant concerns,” the Banks bent to the task of building the APIs, and Open Banking emerged.

Closing

Without the influence of innovators like Gulamhuseinwala and Gibson—along with their willingness to participate in policy and politics—I don’t think the EU’s vision of standardizing interbank information transfer would have resulted in Open Banking. It would have been standardized but decidedly closed like what The Clearing House has done with Real Time Payments in the US. This feat, combined with the EU’s recent momentum in regulation after having taken on the impressive task of pulling 27 countries together into a single economic and political unit, allowed for the fertile ground that has given the EU notable advantages in banking innovation over its friends on the other side of the pond.

Next year, in the US, real time payments might become available to more organizations by way of the FedNow service. The Federal Reserve does not have the same power to push Open Banking rules and regulations that the European Commission enjoys, so it remains to be seen what the level of bank participation and non-bank access will be in the system. Fintechs are clamoring to get on board, and we at Kelsus would love to help with some implementations, so please let us know if you’d like to discuss.

Thanks for reading! Let me know if you think of this post next time watch a panel of experts and you see one of those knowing smirks from a fintech CEO.

—Jon Christensen